Clean Hydrogen Working Group

Hydrogen is a versatile zero-emission energy carrier with significant potential to decarbonize multiple economic sectors. The clean hydrogen working group convenes leading companies across the hydrogen ecosystem, including current and prospective hydrogen consumers, producers, energy companies, capital providers, and other key stakeholders. Recognizing the diversity of hydrogen production pathways, the working group supports the use of hydrogen from all production methods that meaningfully reduce the carbon intensity of gray hydrogen, i.e., hydrogen produced from natural gas without the use of carbon capture, utilization, and storage.

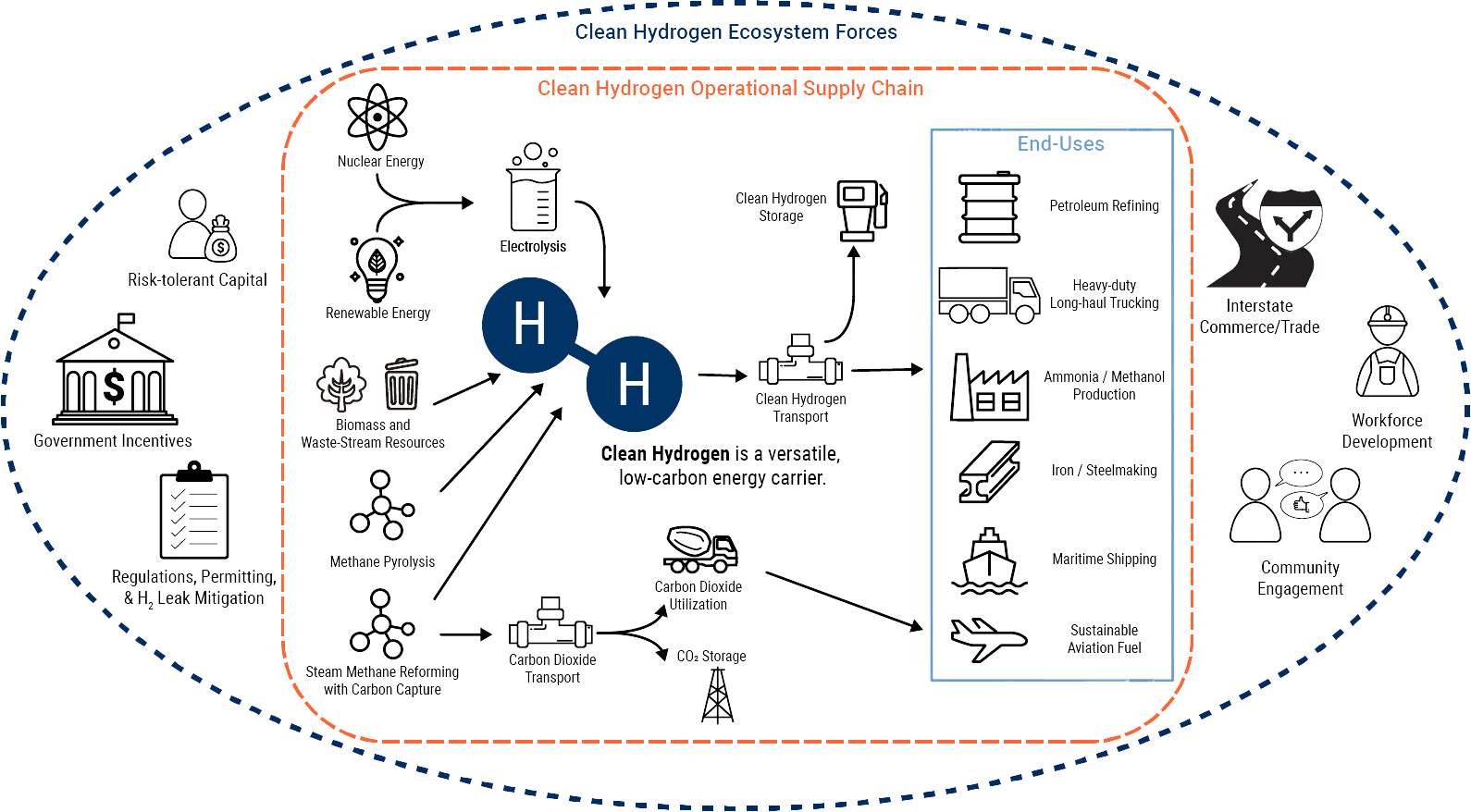

Virtually all the hydrogen used in the United States today is generated through an emissions-intensive process that, while relatively inexpensive, emits significant greenhouse gases. Roughly 90 percent of current hydrogen demand is concentrated in the end uses of petroleum refining, and ammonia and methanol production. Replacing this demand with cleaner hydrogen will significantly reduce emissions in the near term. In addition, full decarbonization will necessitate the development and deployment of new clean technologies and low- and zero-carbon fuels as substitutes in emissions-intensive sectors. In particular, the aviation, maritime, and heavy-duty long-haul transport industries are limited in their ability to directly substitute emissions-intensive fuels and feedstocks with clean electricity and could benefit greatly from the use of cleaner hydrogen as a versatile, low-carbon energy carrier.

Despite a wide spectrum of existing and prospective use cases, demand for cleaner hydrogen continues to stall. Existing gray hydrogen users in the United States have no financial incentive to procure cleaner hydrogen because doing so would greatly exceed the costs of their current supply, much of which they produce themselves. New clean hydrogen demand faces a range of barriers, including ineffective price signals, nascent transportation and storage infrastructure, and a lack of commercial-scale technology demonstrations.

Maximizing the potential of clean hydrogen as a climate solution will necessitate scaling production to ten million metric tons (MMT) annually by 2030, 20 MMT annually by 2040, and 50 MMT annually by 2050. Successfully achieving emissions reductions with clean hydrogen will require the shifting of gray hydrogen production and consumption toward cleaner hydrogen sources. Simultaneously, new demand will need to be created for heavy-emitting use cases. Public policy can play a key role in addressing these challenges to help unlock private sector demand for clean hydrogen.

- Create a venue for current and prospective hydrogen users, producers, supporting infrastructure providers, and sources of capital to learn from each other and collaborate on the solutions needed to address the challenges laid out above.

- Identify barriers and solutions to the uptake of clean hydrogen on the demand-side with a focus on near-term applications, including fuel switching (i.e., from legacy gray hydrogen or natural gas to clean hydrogen) and emerging use cases (e.g., power-to-liquid transportation fuels).

- Align, to the extent practicable, on a shared vision for policy to support rapidly increasing clean hydrogen demand and collectively work towards the enactment of those policies.

- Strengthen connectivity and collaboration across the innovation ecosystem.

The Clean Hydrogen Ecosystem

The Clean hydrogen ecosystem includes key components of the supply chain as well as important ecosystem forces. The ecosystem forces include key local, market, and government factors that will influence the long-term success of the clean hydrogen industry. Clean hydrogen” refers to hydrogen with a carbon intensity not greater than 4 kilograms of carbon dioxide per kilogram, and can be produced through multiple pathways, including steam methane reforming (SMR) with carbon capture (blue hydrogen), electrolysis (green or pink hydrogen, if powered by renewable or nuclear energy respectively), and methane pyrolysis (turquoise).

Clean Hydrogen: Demand-Side Support Policy Recommendations

Achieving deep emissions reductions across the U.S. economy will require rapid development and deployment of new clean technologies and low/zero-carbon fuels, especially in hard-to-decarbonize sectors like refining, chemicals, aviation, maritime, and heavy trucking. Clean hydrogen can serve as a versatile, low-carbon energy carrier to help decarbonize these hard-to-abate applications through its use as a fuel, feedstock, and energy storage medium. Explore our new policy recommendations to expand clean hydrogen demand.

Read Brief

C2ES’s Clean Hydrogen Working Group Highlights 5 Keys to Grow Demand

C2ES staff reflect on five key federal policy recommendations to boost demand for clean hydrogen, addressing funding, infrastructure, market incentives, and carbon pricing to help decarbonize hard-to-electrify sectors.

Read Blog

Room for improvement: Digging into Treasury Hydrogen guidance

In December of 2024, the Treasury Department released its much-anticipated guidance for the 45V Credit for Production of Clean Hydrogen, which recognizes four tiers of tax credits based on the carbon intensity of the hydrogen produced. Once finalized, the guidance will add welcome certainty for participants in seven recently selected Hydrogen Hubs across the country and for many others planning to utilize this promising energy carrier. Explore this blog for insights on the Treasury’s guidance.

Read Blog

Hydrogen Hubs seek to build on regional US strengths

The U.S. Department of Energy has selected seven regional clean hydrogen hubs for federal funding, aiming to accelerate clean hydrogen adoption across various sectors nationwide. C2ES Innovation Manager Johanna Wassermann reflects on how the model addresses some of the key market challenges for hydrogen.

Read Blog